The Financial Accounting Standards Board (FASB) and the International Accounting Standards Board (IASB) have been working towards a single comprehensive revenue recognition standard since the initial joint project was put together in 2002. The objective of the joint effort was to:

- Remove inconsistences and weaknesses in the existing revenue recognition frameworks

- Provide a more robust framework for addressing revenue issues

- Improve comparability across entities, industries, jurisdictions, and capital markets

- Provide more useful information to financial statement users through enhanced disclosures

- Simplify financial statement preparation by streamlining and reducing the volume of guidance

The joint effort culminated in the issuing of the new revenue standards by both boards in 2014. ASC 606: Revenue from contracts with customers, issued by FASB and IFRS 15: Revenue from contracts with customers issued by IASB. The initial standards issued in 2014 have been severally amended and updated by both boards in response to industry input, with the most recent amendment issued by FASB in December 2016. While the standards are largely converged, some material differences remain.

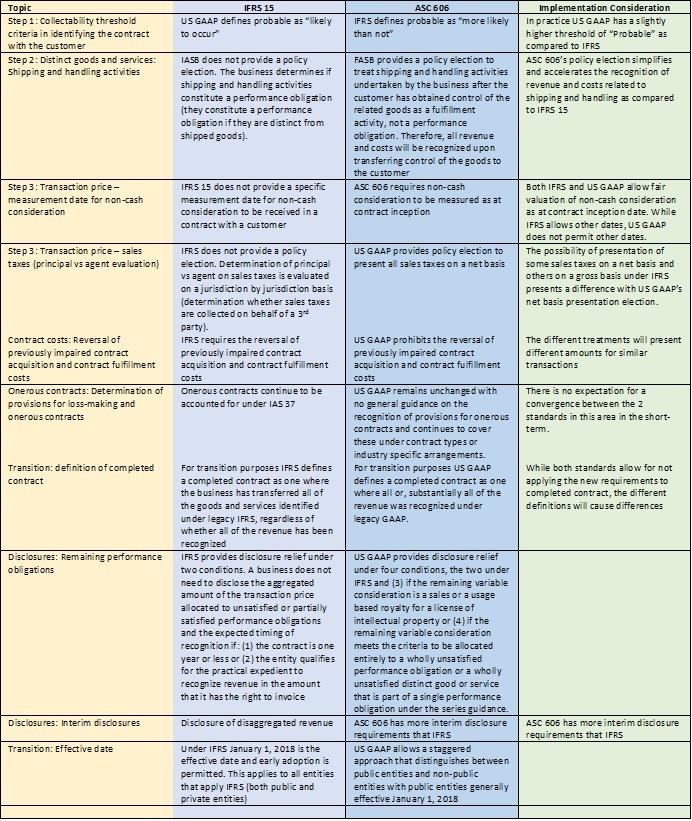

ASC 606 – IFRS 15 Differences

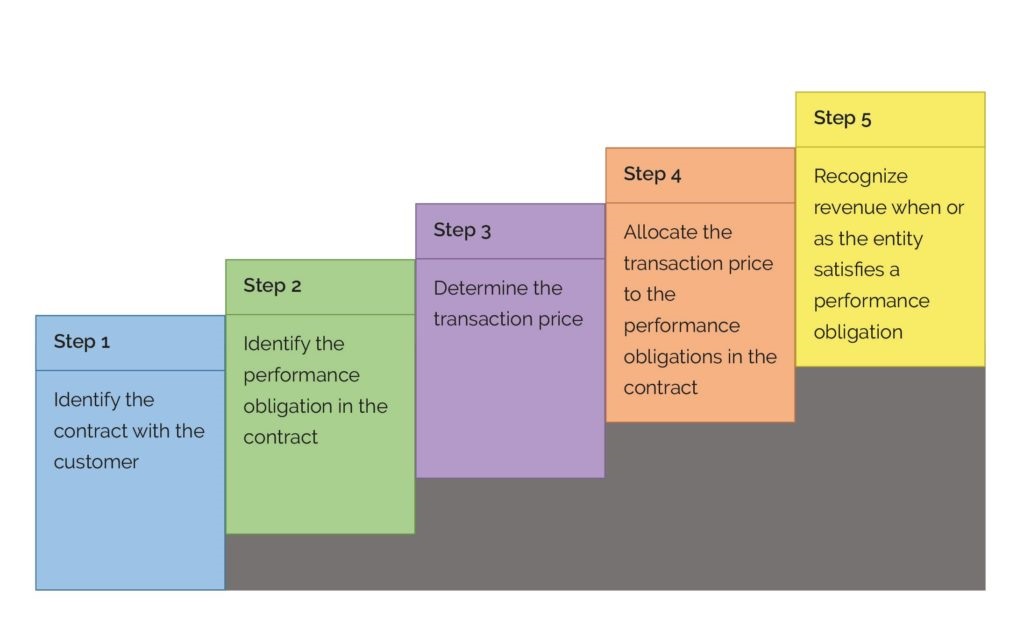

The core principle of ASC 606 is to recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services. Both FASB and IASB have adopted a five-step approach to support this core principle.

ASC 606: Five-step model

Step 1: Identifying the contract with the customer

- All parties have approved the agreement. Contracts may be written, oral, or implied by the entity’s normal business practice.

- All parties are committed to fulfilling their obligations. The standard states that if each party has the unilateral right to terminate a wholly unperformed obligation, then no contract exists.

- Each party’s rights are identifiable. The contract arrangement must clearly identify the goods or services to be provided. The ability to identify performance obligations is a prerequisite for determining when the transfer of control has occurred.

- Payment terms are identified. An entity cannot determine the transaction price if the payment terms for the goods or services is not known. The overriding principle is that there must be an enforceable right to receive payment in exchange for goods or services.

- The contract has commercial substance. A contract has commercial substance if the risk, timing or amount of the entity’s future cash flows will change as a result of the contract. If there is no change, it is unlikely that the contract has commercial substance.

- Collectibility is probable. The objective of the collectibility assessment is to determine whether there is a substantive transaction between the entity and the customer. The assessment must demonstrate both the customer’s ability and intent to pay amounts as they become due.

Entities need to consider the following when addressing Step 1 requirements:

When an entity receives payment from an agreement that does not qualify as a contract the entity may only recognize revenue when one of the two conditions below is met:

- The agreement has been terminated and payment received is nonrefundable

- The entity does not owe any goods or services to the customer, and all, or substantially all, of the transaction price has been received and is nonrefundable.

Combining contracts

An entity is required to combine multiple contracts with the same customer into one contract if at least one of the following conditions is met:

- Contracts are negotiated as a single package with one business objective

- The payment amount for one contract is dependent on the performance of the other contract

Portfolio approach

FASB provides the portfolio approach as a practical expedient that an entity may use in accounting for a group of contracts if the entity reasonably expects that there will be no material difference had the contracts been accounted for individually.

Contract Modification

A contract modification may change the scope or price of the contract or both. A contract modification exists when parties to the contract agree to the modification either in writing, orally, or based on the parties’ customary business practices.

Step 2: Identifying the performance obligations in the contract

A performance obligation is a promise to provide a distinct good or service or a series of distinct goods or services as defined by the standard. Performance obligations constitute the unit of account for purposes of applying ASC 606, and therefore determine when and how revenue is recognized. A good or service distinct when:

- The customer can benefit from the good or service, and

- The good or service can be transferred independent of other performance obligations in the contract

Principal vs Agent (Gross vs Net)

When multiple unrelated parties contribute to the provision of goods or services to a customer, the entity must determine whether its performance obligation is to provide the goods or services itself (as a principal) or arrange for other parties to provide the goods or services (as an agent). If the entity is a principal in the arrangement it will recognize the gross amount. However, if the entity is the agent in the arrangement it will recognize the net amount.

Warranties

Entities typically provide warranties for goods and services that are sold to customers. ASC 606 identifies two types of warranties:

- Assurance-type warranties. Warranties that only guarantee that the good or service will function as promised. Assurance-type warranties do not create separate performance obligations.

- Service-type warranties. These are warranties that provide a service in addition to assurance. Service-type warranties create separate performance obligations.

Customer options for additional goods or services

Entities often provide options for customers to purchase additional goods or services in the future such as a discounted renewal of a contract. A customer option that provides a material right to the customer creates a separate performance obligation.

Nonrefundable upfront fees

Nonrefundable upfront fees are common in some industries such as activation fees in telco contracts. If no good or service is transferred to the customer the arrangement does not create a separate performance obligation, however if a good or service is transferred then a separate performance obligation is created.

Stand Ready obligations

An entity must determine whether its promise to provide goods or services is a stand ready promise. An example of a stand ready promise is when an entity promises to provide unspecified upgrades to a software arrangement when and if required.

Right of return

While a right of return in an arrangement is not a separate performance obligation, it is critical in the evaluation of the price of the good or service that is transferred. Revenue is recognized for goods that are not expected to be returned.

Step 3: Determine the transaction price

ASC 606 guides that the transaction price is the amount of consideration to which an entity expects to be entitled in exchange for transferring promised goods or services to a customer, excluding amounts collected on behalf of third parties (for example, some sales taxes). The consideration promised in a contract with a customer may include fixed amounts, variable amounts, or both.

The transaction price is easy to determine where a contract is for a fixed amount of consideration in return for a fixed number of goods or services in a reasonably short timeframe. Complexities arise where a contract includes any of the following:

Variable consideration

Consideration is variable when the amount of consideration is subject to change due to timing, performance, or other factors. Variable consideration can come from discounts, rebates, refunds, credits, incentives, and other similar items. While the method used to determine variable consideration is not a policy choice, the entity must use the method that best predicts the amount of consideration to which the entity will be entitled based on the terms of the contract. The selected method used should be applied consistently throughout the contract.

Significant financing component

In determining the transaction price, an entity shall adjust the promised amount of consideration for the effects of the time value of money if the timing of payments agreed to by the parties to the contract (either explicitly or implicitly) provides the customer or the entity with a significant benefit of financing the transfer of goods or services to the customer.

Noncash consideration

Noncash consideration must be measured as of the date of inception of the contract. The fair value of the noncash consideration is included in the transaction price. Where fair value is not readily determinable, the standalone selling price of the goods or services transferred is used.

Step 4: Allocate the transaction price

The standard requires that the transaction price must be allocated to each performance obligation based on the relative standalone selling prices of the goods or services being provided to the customer. The best evidence of a standalone selling price is the price an entity charges for that good or service when the entity sells it separately in similar circumstances to similar customers.

Step 5: Recognize revenue when or as performance obligations are satisfied

ASC 606 requires that an entity shall recognize revenue when (or as) the entity satisfies a performance obligation by transferring a promised good or service (that is, an asset) to a customer. A performance obligation is satisfied at a point in time if it meets the following criteria or does not meet the criterial for performance obligations satisfied over time:

- The entity has a present right to payment

- The customer has legal title

- The customer has physical possession

- The customer has the significant risks and rewards of ownership

Determining if a performance obligation is satisfied over time

Entities are required to determine, at the inception of the contract, if a performance obligation is satisfied over time. A performance obligation that is not satisfied over time is assumed to be satisfied at a point in time. A performance obligation is satisfied over time if it meets any of the following criteria:

- The customer simultaneously receives and consumes the benefit provided by the entity as the entity performs

- The entity’s performance creates or enhances assets that the customer controls while the assets are being created or enhanced

- The performance does not create an asset with an alternative use to the entity, and the entity has an enforceable right to payment for performance completed to date

Measures of progress over time

An entity must measure progress towards the satisfaction of a performance obligation in a pattern that reflects the transfer or control of the promised goods or services to the customer. Allowed measurement methods include:

- Output methods, where revenue is recognized based on direct measurement of the value transferred to the customer

- Input methods, where revenue is recognized based on the entity’s efforts to satisfy the performance obligation

Presentation and disclosures

Entities are required to present contract assets, contract liabilities and receivables due from customers separately in the statement of financial position.

Disclosures must include sufficient information to enable users of the financial statements to understand the nature, timing and uncertainty of revenue and cash flows arising from contracts with customers. Disclosures must include:

- Contracts with customers

- Significant judgment, and changes in the judgements, made in applying the ASC 606 to those contracts

- Assets recognized in respect of costs of obtaining or fulfilling contracts.

Implementing the new standard will be a significant project and will require a strong team to see it through. Most businesses will need to strengthen their internal teams with outside experts to deliver an effective implementation of the standard. As the effective date gets closer there will be increased pressure and competing demands for both internal and external ASC 606 implementation resources. The best approach is to start now.

How we can help

Our team offers a broad range of experience and deep technical expertise in US GAAP and IFRS implementation and accounting solutions. Our professionals deliver world class US GAAP and IFRS implementations and advisory services in the US, Canada and around the world. We can help your business with planning, analysis, implementation, and ongoing support related to ASC 606, IFRS 15 and other unique accounting solutions that your business may need.

Howlite Consulting Inc.

www.howliteinc.com

info@howliteinc.com

+1 587 317 4481

Post a Comment:

You must Register or Login to post a comment.